Anytime. Anywhere.

SavvyMoney gets you your credit score. And more.

Staying on top of your credit has never been easier.

With one powerful tool, access your credit score, full credit report, credit monitoring, financial tips, and education—all without impacting your credit score.

As a Credit Union ONE member, you can start using SavvyMoney for free by logging in to Digital Banking!

Money Management Tips

Credit Score FAQ

A credit score is a three-digit number calculated to indicate your creditworthiness. The higher the score, the more creditworthy you are to a lender. A credit score is calculated from the information in your credit report and considers your on-time payments, the length of your payment history, your mix of different types of credit accounts, and other such factors. It is important to know that your score does not take your age, income, employment, marital status, or your bank account balances into account.

You can learn more about credit scores and scoring models from the Consumer Financial Consumer Financial Protection Bureau website.

VantageScore® was founded by the 3 leading credit reporting agencies: Experian, Equifax, and TransUnion. This credit score model was developed by a representative team of statisticians, analysts, and credit data experts from each of the credit reporting companies, and is used by hundreds of institutions, including credit unions, banks, credit card issuers, and mortgage lenders.

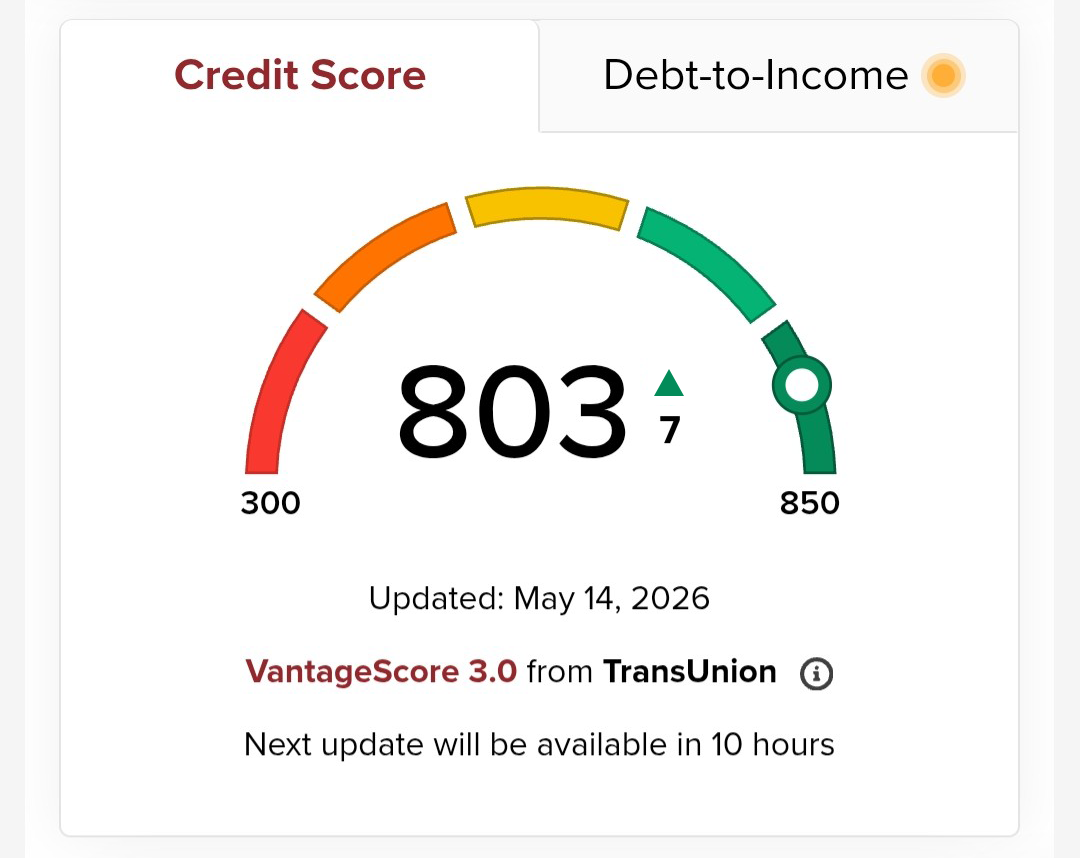

The VantageScore® 3.0, the score that is shown in SavvyMoney, is a newer and more popular version of VantageScore®. It is calculated on a scale of 300-850, with 300 being the lowest score and 850 being the highest score.

A good score may mean you have easier access to more credit and lower interest rates. The consumer benefits of a good credit score go beyond the obvious. For example, underwriting processes that use credit scores allow consumers to obtain credit much more quickly than in the past.

40% Payment History

Repayment behavior by paying bills on time to avoid delinquency. More recent or multiple late payments can hurt your score.

21% Depth of credit

Depth refers to the ages and types of credit accounts you have. Lenders typically prefer individuals with long-term and varied accounts.

20% Credit Utilization

This refers to the percentage of your total credit used from the total credit available to you. Lenders generally see credit utilizations under 30% more favorably.

11% Balances

The total amount of recently reported balances. Keep the amounts you owe low by paying off monthly balances.

5% Recent Credit

The number of recently opened credit accounts and credit inquiries.

3% Available Credit

The amount of credit available to you. Lenders consider how much credit you have available. Keeping this amount high shows responsible spending.

One of the most important misperceptions about credit scores is what information the VantageScore® model, or any credit scoring model for that matter, is NOT used. The VantageScore® model does not consider race, color, religion, nationality, sex, marital status, age, salary, occupation, title, employer, employment history, where you live or where you shop.

Building Credit FAQ

- Pay Your Bills on Time, Every Month. Payment history is the largest factor in your credit score.

- Apply for Credit Only When You Need It. Try not to open too many accounts too frequently. These frequent inquiries can ding your credit.

- Keep Your Outstanding Balances Low. Keep balances below 30 percent of the credit limit on each of your revolving accounts.

- Reduce Your Total Debt. It is not necessarily bad to have debt as long as it’s manageable. Too much debt at high interest rates can get out of hand if a financial emergency comes up. Consider paying down some of your outstanding loans.

- Build Up Credit History.Maintaining a timely payment history for a mix of accounts (e.g. credit cards, auto, mortgage) over a long period can improve your score.

Since the single most important factor in credit score is payment history, using credit and paying off your balances on time will have the greatest impact on your score. Carrying a balance every month may incur interest charges, so if you can, pay off the cards in full and on time.

The best way to build a solid credit score is to manage all your accounts properly. Best practices include paying all your credit obligations on time every month, applying for credit only when needed, and keeping balances on credit cards as low as you possibly can if you cannot pay them in full each month.

When you close a credit card account, you lose the value of that card’s credit limit in the credit usage calculation. The credit limit is an important component when determining a consumer’s balance to credit limit or the “credit usage” ratio. This ratio rewards consumers who have low credit card balances relative to their credit limits.

If you close credit cards, especially those with large credit limits, you will likely cause your credit usage ratio to go up (if you carry balances). This can cause your score to go down considerably.

Additionally, if you close credit card accounts, the credit bureaus will eventually remove them from your credit reports. Even though it can take years for an account to be removed from your credit reports, once it is gone you will get no credit for your responsible management of that account.

The quantity of loans is not as important in credit scoring as the quality of how well those accounts are managed. In other words, your score is more positively impacted by keeping loans in good standing without missing payments.

Consumers are encouraged to shop for the best loan rates and conditions. Accordingly, the VantageScore® model does not penalize multiple inquiries made within a short period. When several inquiries are made within a shortened timeframe, it is assumed that the consumer is shopping around for a rate and not opening multiple lines of credit.

The VantageScore® model uses a 14-day rolling window in which all credit inquiries within that window are considered one inquiry regardless of the type of account. So regardless of whether the credit inquiry is made in response to a mortgage, auto, or bank credit card application, it will be counted only once during that 14-day window.

Credit reports reflect your credit activity. The quantity of cards is less important than how you manage your credit cards. It’s generally a good idea to have a limited number of credit cards so that you can keep low balances, with a good payment history, over a long period.

Paying off debts does not automatically boost your score. While your credit card and other loan balances may be low because of a recent payment, due to the lenders’ reporting cycles, it may take some time for the payments to be reflected in your credit score. Moreover, available credit and balances are only one of several other factors that are considered by credit score models. Improving your credit score can be achieved over time by regularly practicing these sound financial management techniques:

- Pay your bills on time

- Apply for credit only when it’s needed; do not open new accounts frequently or open multiple accounts within a short period.

- Keep your outstanding balances low. A good rule of thumb is not to exceed 30% of your available credit limit with each account.

- Pay any delinquent accounts as soon as possible and then keep them current.